Home prices in the U.S. are rising to new levels, even surpassing pre-crisis levels in some metros, but home prices in the U.S. are relatively low compared to other developed nations.

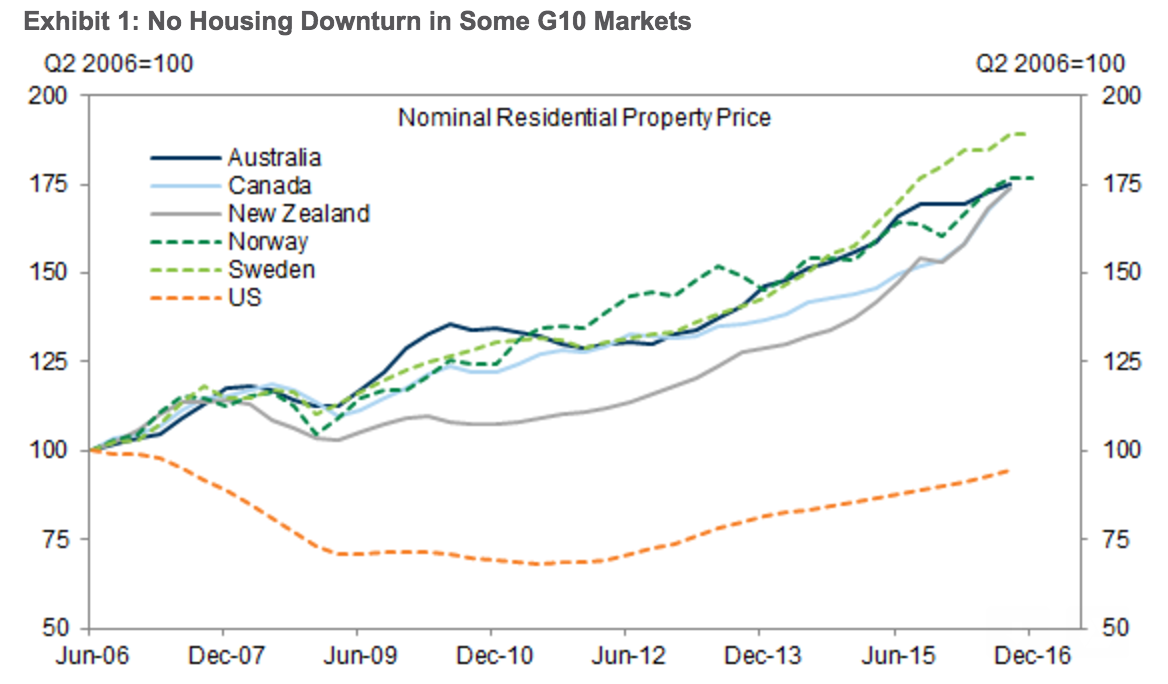

Over the past few years in the U.S., home prices peaked in July 2006, troughed in February 2012 and have since returned to pre-crisis levels once again. However, this wasn’t the case for other developed nations. Other G10 economies never saw a downturn, and have continued increasing.

The Group of Ten is made up of eleven industrial countries (Belgium, Canada, France, Germany, Italy, Japan, the Netherlands, Sweden, Switzerland, the United Kingdom and the United States) which consult and co-operate on economic, monetary and financial matters.

Now, some are concerned about broader consequences if the real estate markets go south, according to a report from Goldman Sachs. The report explains there are no imminent problems in G10 markets, but current imbalances could worsen cyclical weakness later.

This chart shows U.S. home prices are far below other G10 markets. In 2006, home prices in the U.S. stood at about the same level as the other countries. However as the recession hit in the U.S., home prices in other G10 nations continued to grow.

Click to Enlarge

(Source: Bank for International Settlements, Goldman Sachs Global Investment Research)

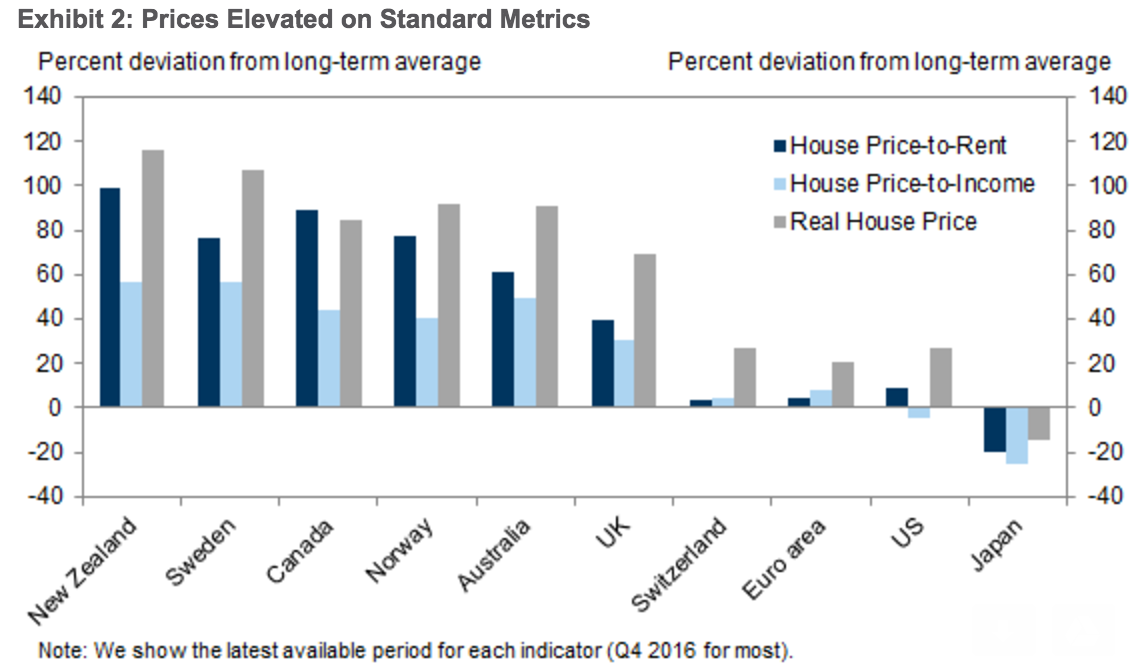

And in fact, home prices in many G10 markets are significantly overvalued. Goldman Sachs compared the ratio of home prices to rent, the ratio of home prices to household income and real home prices, home prices deflated by a consumer price index.

This chart shows New Zealand is the most overvalued G10 nation. For comparison, the in the U.S. in 2006 the price-to-income ratio and price-to-rent ratios were about 15% and 30% above their long-run averages, respectively.

Click to Enlarge

(Source: OECD, Goldman Sachs Global Investment Research)

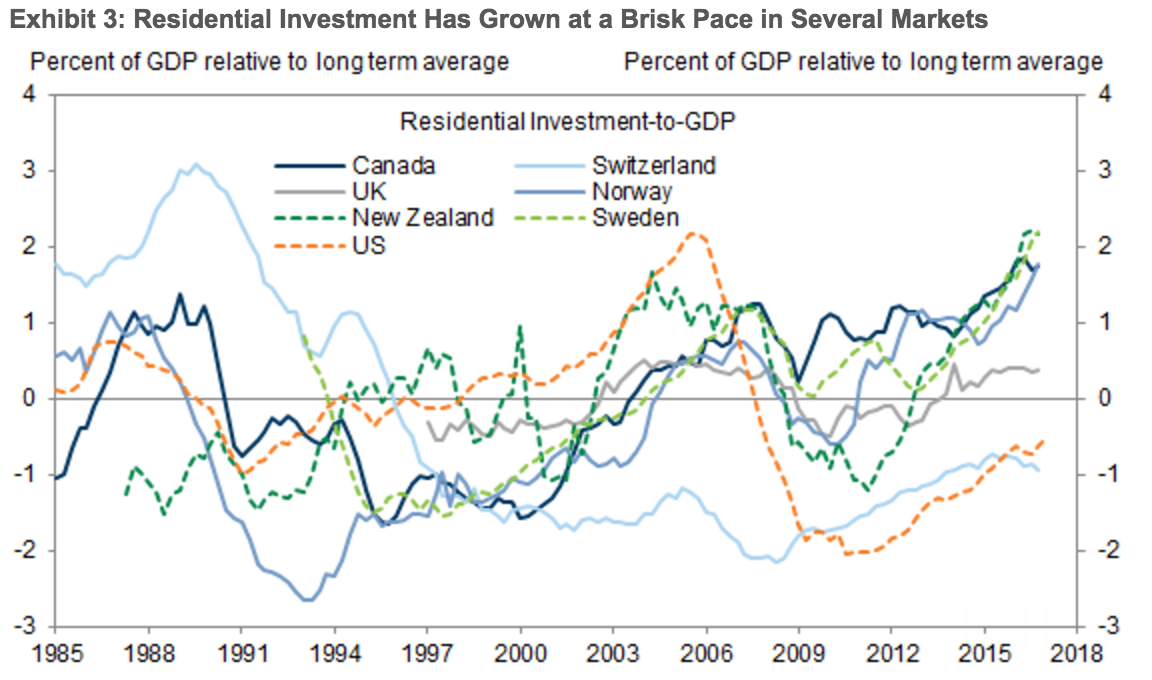

Goldman Sachs calculated the underlying demographic trend in household formation by dividing the change in the resident population by the average number of persons per household. It then compared the five-year average of this estimate with the five-year average of housing starts. The company could then determine whether building activity is high due to faster population growth.

Click to Enlarge

(Source: Haver Analytics, Goldman Sachs Global Investment Research)

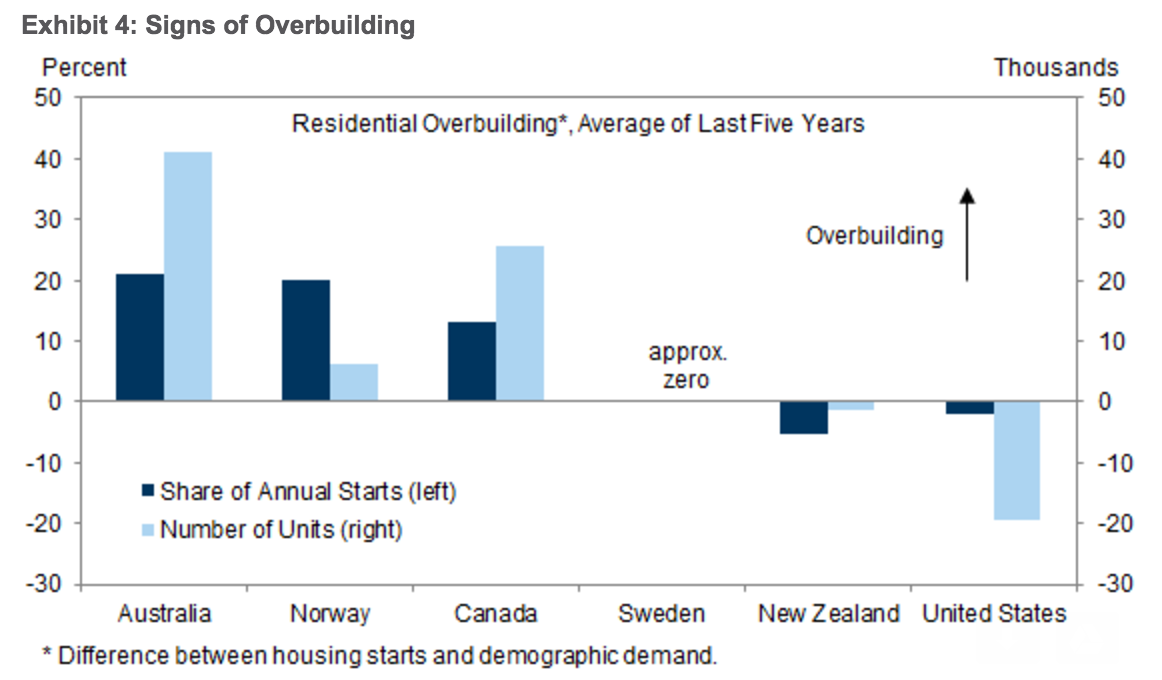

It might come as no surprise that the U.S. is underperforming when it comes to new construction. Other countries, such as Australia, are overbuilding.

Click to Enlarge

(Source: Haver Analytics, Goldman Sachs Global Investment Research)

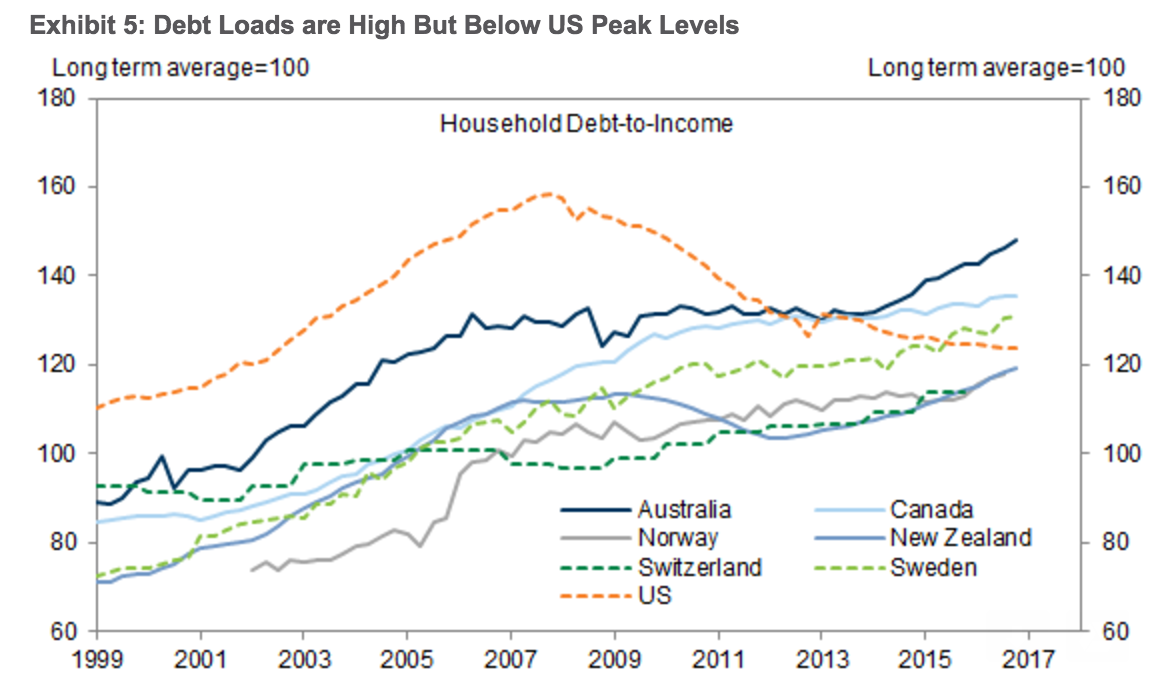

But despite falling significantly below other G10 nations in home price categories, the debt-to-income ratio in the U.S. falls higher. The U.S. comes in fourth when it comes to mortgage debt, but remains significantly below peak values.

Click to Enlarge

(Source: Haver Analytics)

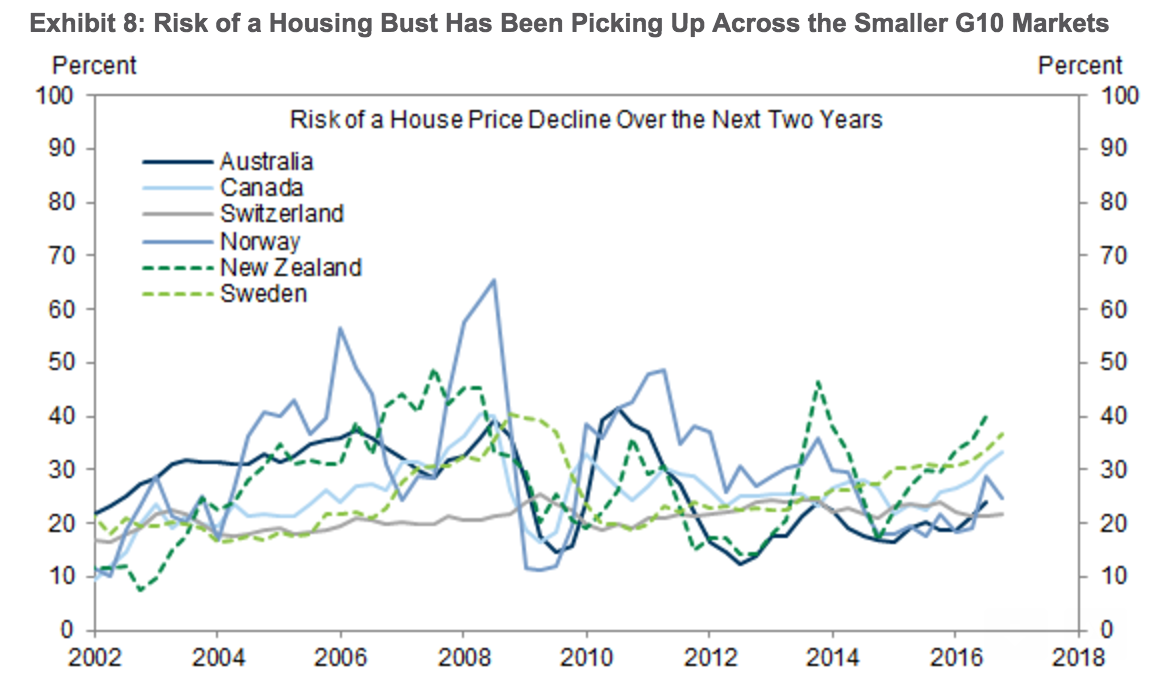

Due to rising home prices and high credit growth, the probability of a housing bust over the next five to eight quarters is the highest in Sweden and New Zealand at 35% to 40%, according to the report. Canada follows closely behind with a probability of about 30%. For the remaining countries, the model-implied probability of a housing bust is around 20-25%.

Click to Enlarge

(Source: Goldman Sachs Global Investment Research)

The Goldman Sachs note was produced by Senior Economist Zach Pandl and Nocholas Fawcett, executive director in the Global Investment Research division.